Part 1: Effectively Managing Your Greenhouse Gas Emissions Inventory

CommercialJan 26, 2022

When organizations seek to reduce their greenhouse gas (GHG) footprint, it’s important that an accurate emissions inventory is created. Implementing a detailed inventory will facilitate effective reporting, target setting, planning, management and tracking of GHG footprint reduction activities and outcomes. In this edition of Customer Insights, we’ll provide an overview of the generally accepted principles surrounding GHG accounting, inventory development and reporting.

The most generally accepted standards and principles for GHG reporting are laid out comprehensively in the Corporate Accounting and Reporting Standard published by The Greenhouse Gas Protocol (the GHG Standard). The Greenhouse Gas Protocol is a collaboration between the World Resources Institute, the World Business Council for Sustainable Development, and various governments, industry organizations, non-governmental organizations (NGOs), businesses and other organizations.

The GHG Standard sets out five principles that should guide the development of an organization’s emissions inventory (the following is taken verbatim from the GHG Standard):

Relevance: Ensure the GHG inventory appropriately reflects the GHG emissions of the company and serves the decision-making needs of users – both internal and external to the company.

Completeness: Account for and report on all GHG emission sources and activities within the chosen inventory boundary. Disclose and justify any specific exclusions.

Consistency: Use consistent methodologies to allow for meaningful comparisons of emissions over time. Transparently document any changes to the data, inventory boundary, methods, or any other relevant factors in the time series.

Transparency: Address all relevant issues in a factual and coherent manner, based on a clear audit trail. Disclose any relevant assumptions and make appropriate references to the accounting and calculation methodologies and data sources used.

Accuracy: Ensure that the quantification of GHG emissions is systematically neither over nor under actual emissions, as far as can be judged, and that uncertainties are reduced as far as practicable. Achieve sufficient accuracy to enable users to make decisions with reasonable assurance as to the integrity of the reported information.

Defining the Boundaries

As referenced in the principles, in order to develop an effective GHG emissions inventory, an organization needs to rigorously define the boundaries within which it is accounting for and classifying its emissions. The boundaries that the GHG Standard contemplates are of two varieties – Organizational and Operational.

The establishment of organizational boundaries determines which emissions an organization will report at all. Organizational boundaries here refer to boundaries of ownership and control of emitting facilities. Though the Standard addresses these topics in detail, the general principle is that organizations should account for facility level emissions to the degree that the organization owns the value associated with activity operations, and/or to the degree that the organization controls the activity operations. The key point here is that organizations need to consider and elect which form of boundary determination is most relevant in their case, and then apply that election consistently.

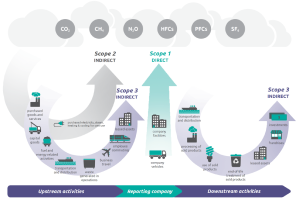

The establishment of operational boundaries of GHG emissions serves to categorize those emissions by the degree to which they stem directly from organizational activities, and by extension the degree to which organizations may affect or influence activities and associated emissions. Here the standard establishes operational boundaries to sort emissions into three distinct ‘Scopes’:

Scope 1: Emissions that are created directly through activities undertaken by the organization within its defined organizational boundaries. This includes emissions generated from combustion associated with facility heating, steam generation, on-site electricity generation, vehicles/transportation; or from other non-combustion processes or activities that result in the formation and emissions of GHGs.

Scope 2: Emissions that arise from electricity that is purchased by the organization.

Scope 3: Emissions that are associated with activities that are either ‘upstream’ of the organization’s operations – such as emissions from production of purchased supplies or services, employee travel, transportation of supplies and fuel – or activities that are ‘downstream’ of the organization’s operations – such as outsourced shipping of sold goods to consumers, product use, product disposal, etc.

Accounting for and developing inventories of both Scope 1 and 2 emissions is generally considered a ‘must’ for any serious GHG reporting and tracking program. Scope 3 emissions are generally considered optional, but may be highly relevant for organizations where outsourcing or purchased supplies is a very important part of operations.

Establish Quality Data Sources and Processes

Once organizational boundaries are set and an understanding of the sources for Scope 1 and Scope 2 (and possibly Scope 3) emissions is set, the next task is to establish sources of activity data for these emissions, along with processes for compiling the data. Primarily for most organizations, this will involve cataloguing sources of fuel consumption data for Scope 1 accounting – such as gasoline, diesel, fuel oil, natural gas, etc. – and sources of electricity consumption data for Scope 2 accounting.

Data quality is of course paramount in satisfying the core accounting principle of accuracy. Organizations need to put a good amount of work into specifying the best possible sources for activity data and in developing robust and fault free process for intake, assembly and aggregation of such data. Particular care needs to be taken at interface and transformation points – i.e., anytime data is moved between systems, translated, or manipulated – as these are the most likely sources of data errors and corruption.

Along with data, the other component required for determining GHG quantities emitted is source and fuel specific emissions factors, such that:

GHG Quantity = Fuel Quantity X Fuel Emission Factor

The emissions factors for any given fuel (here we refer to electricity as a fuel) will vary by region and supplier of the fuel. Where possible, organizations should obtain accurate emissions factors from the suppliers of fuel. However, organizations should also determine the basis of the emission factor provided by suppliers. If supplier specific emissions factors are not available (or are determined to be unreliable), credible public sources exist for these factors (referenced in the Standard or on the GHG Protocol website).

Establishing the Baseline Year

A final basic consideration for an effective GHG accounting and reporting program is the establishment of a Baseline Year. The Baseline Year is the standard against which ongoing GHG management efforts will be managed, and so should be chosen to accurately and fairly represent an organization’s starting point in its GHG footprint management activities. The Baseline Year will typically also serve as a standard for any GHG reduction targets that the organization will establish and work towards. An important consideration outlined in the GHG Standard is that organizations need to recalculate Baseline Year emissions any time there is a substantial change in the nature of their business owing to acquisition or divestiture of business activities.

Additionally, with regard to Scope 2 emissions in particular, the GHG Standard calls for the Fuel Emissions Factors to be accounted for by separately two methods, as described in more detail in the GHG Protocol Scope 2 Guidance:

Location-Based Method: ‘A method to quantify Scope 2 GHG emissions based on average energy generation emission factors for defined geographic locations, including local, subnational, or national boundaries. Emission factors representing average emissions from energy generation occurring within a defined geographic area and a defined time period.’ (from the Corporate Standard)

Market-Based Method: ‘A method to quantify the Scope 2 GHG emissions of a reporter based on GHG emissions emitted by the generators from which the reporter contractually purchases electricity bundled with contractual instruments, or contractual instruments on their own’ (from the Corporate Standard). The contractual instruments referred to here may be Renewable Energy Certificates (RECs), Power Purchase Agreements (PPAs), Integrated Retail Products, or other qualifying instruments. Each of these needs to meet Quality Criteria laid out in the Corporate Standard.

Underlying all of these activities again are the principles laid out above – Relevance, Completeness, Consistency, Transparency and Accuracy. While the process of developing a comprehensive GHG inventory and establishing reporting procedures can be daunting, guidance by and adherence to these principles can ensure that organizations avoid pitfalls and risks and capture the benefits associated with effective management of their GHG emissions footprint.

Organizations that fail to effectively manage their GHG profile face the risk of getting left behind by competitors/peers, spurned by stakeholders, or worse. The first step in effective management is getting a good grasp on where you are today through a solid inventory. We can help you take that first step.

Interested in taking the first step?

In the current environment, understanding your organization’s Scope 1 and Scope 2 GHG emissions footprint is a critical first step in protecting your organization from risks and realizing value.

AEP Energy is uniquely qualified to help you establish your emissions inventory and to support progress toward your GHG management goals. Our experienced Services professionals can help guide you down the right path – to get started, If you are already working with an AEP Energy Sales Representative, they will happily provide more information, or you can click here to request more information.

AEP Energy does not guarantee the accuracy, timeliness, suitability, completeness, freedom from error, or value of any information herein. The information presented is provided “as is”, “as available”, and for informational purposes only, speaks only to events or circumstances on or before the date it is presented, and should not be construed as advice, a recommendation, or a guarantee of future results. AEP Energy disclaims any and all liabilities and warranties related hereto, including any obligation to update or correct the information herein. Summaries and website links included herein (collectively, “Links”) are not under AEP Energy’s control and are provided for reference only and not for commercial purposes. AEP Energy does not endorse or approve of the Links or related information and does not provide any warranty of any kind or nature related thereto.

3 min read Let’s talk about something that’s making waves in the energy sector: demand management. Specifically, how it can help businesses navigate the rising capacity prices in PJM. Whether you’re a business owner or an operations manager, you’ll want to pay attention to this. What is Demand Management? Demand management is a strategy where …

In the ever-evolving landscape of energy markets, a significant development has emerged from Pennsylvania. Governor Josh Shapiro and PJM Interconnection have reached a pivotal agreement aimed at protecting consumers from steep electricity price hikes. This agreement is not just a win for Pennsylvania but for the entire PJM region, which spans 13 states and the …

Enter your zip code to see energy plans in your area

Already an AEP energy customer?Login to view account details or enroll at the same rate as new customers.

We found several utilities in your area! Please select yours below:

AEP Energy Reward Store is filled with a variety of energy-saving products for your home. It is a simple and convenient way for you to shop for items to make your home more energy efficient while saving you time and money.

Collect Reward Dollars each month ($5/electric, $3/natural gas) for simply being an AEP Energy Customer.

Shop AEP Energy Reward Store for energy-efficient products like smart thermostats, LED lighting, and more.

Redeem your accumulated Reward Dollars and enjoy smart solutions for your home.

We're Sorry

Brandi Nye, Managing Director of Business Solutions

Brandi is an expert in her field with professional experience in the sustainability industry. Not only does Brandi have solid base knowledge, but she continues to grow her acumen through various learning and development experiences. Brandi is a creative and thoughtful utility professional with expertise in regulatory and utility operations.