April 2018 Edition: Natural Gas: What’s in store for 2018.

In this edition we’ll review several key factors that influence natural gas prices; weather, storage inventories, and market demand. Read this edition to learn more about these fundamentals and how their outlooks affect forward natural gas prices.

If you’re in charge of purchasing energy for your business, you know how important it is to stay on top of energy trends. In this article, we’ll take a look at the specific demand drivers of natural gas and how these may impact natural gas prices this summer. There are several key factors that influence natural gas demand: weather, storage inventories, and market demand. We will discuss each of these fundamentals and how their outlooks affect forward natural gas prices.

Weather

The first, and arguably most important driver of natural gas prices is weather. Natural gas demand is driven by the need to either heat or cool commercial, industrial or residential structures when temperatures are at extremes. Weather by its nature is the most challenging to forecast. Ironically, weather is also the largest driver of demand, and therefore, probably has the most direct, real-time impact on natural

gas prices.

Weather forecasts beyond three to five days are subject to high degrees of uncertainty. For this reason, many long-term forecasts focus on trends that may influence future temperatures. Recently, the National Weather Service provided its long-term outlook for the period of April 2018 through March 2019, which projects a high probability of above normal temperatures for much of the United States. Exceptions to that forecast are seen in the Central and Northern Plains and the Pacific Northwest as these regions are forecasted to experience an equal chance of above, below, or normal temperatures. The very generic nature of that forecast speaks to the lack of clarity and actionable information provided by long-term weather forecasts.

Storage

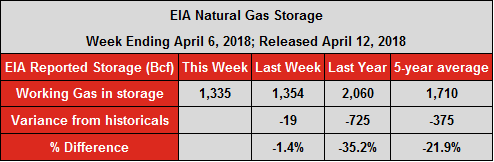

Another important market fundamental that influences natural gas pricing is storage inventories. Natural gas storage inventories are highly correlated to weather. In winter months, natural gas inventories decrease significantly during periods of extreme cold. Each Thursday morning, the EIA reports week-ending storage inventory levels along with comparisons against inventories at the same time in the prior year, and, the five-year average.

Natural gas prices react real-time to the Thursday storage report as market participants interpret how storage levels may impact demand going forward. For instance, during a week of heavy storage withdrawal, prices tend to go up as less supply is available to get through the peak demand season. Less natural gas available to pull from storage means a greater need for natural gas purchases and deliveries during periods of sustained cold. Below find an example of a weekly storage report published by the EIA.

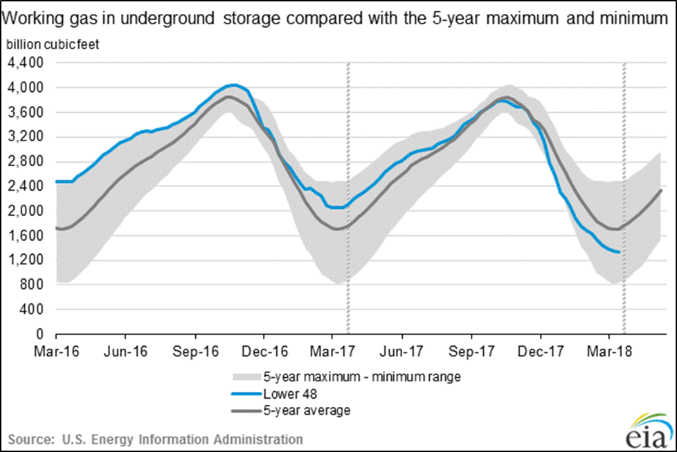

From a historical perspective, natural gas supply outpaces demand in the months of April through October and lags behind demand in the months of November through March. Because of this seasonal supply, storage plays an important role in keeping the natural gas market balanced. With the calendar just about to flip to the traditional injection season, it is expected that natural gas will end the winter withdrawal season with approximately 1,340 billion cubic feet (Bcf) in storage. The current expected inventory trough of 1,340 Bcf is approximately 720 Bcf lower than levels from early April 2017. This is a product of a current winter that has been much cooler than the extremely mild winter of 2016 – 2017. This level also is approximately 370 Bcf lower than average inventory levels for early April over the past five years.

The five-year average for inventory levels at the end of the injection season is 3,848 Bcf. The benchmark for a generally accepted comfortable injection season ending storage is 4,000 Bcf. Therefore, the market needs to inject 2,508 Bdf over the summer months to reach the five-year average level by the end of October 2018 and 2,660 Bcf to get to hit the 4,000 Bcf benchmark. The increased demand required to make up for lagging storage inventories represents approximately 370 Bcf in incremental demand during the 2018 summer and storage injection season. That represents roughly 3.08 Bcf in increased daily demand.

Market Demand

Two areas that have had a dramatic impact on natural gas demand over the past several years have been the continued growth of natural gas as an input for power generation and the exporting of liquefied natural gas (LNG) from the Gulf Coast and Mid-Atlantic regions of the U.S. It is expected that the upcoming summer will see over 7,000 MW of coal-fired power removed from the nation’s portfolio of electric generation. Natural gas fired generation is expected to replace much of that supply. The anticipated increase in natural gas fired generation is expected to produce a 2.5 Bcf per day increase in natural gas demand during the summer of 2018. LNG exports have also continued to ramp up over the past year from both increased operations at the Sabine Pass terminal in Louisiana and the commissioning of the Cove Point facility in Southern Maryland in March of 2018. Increased operations at these two facilities are expected to increase demand for natural gas by approximately 1.5 Bcf per day.

Increased LNG exports, expansion in the United States’ natural gas generation fleet and making up for lagging storage inventories will combine to create an increased demand for natural gas this summer in a range of 5.7 to 7.08 Bcf per day. Daily demand for natural gas was approximately 74 Bcf per day throughout 2017. The anticipated increase in demand for the summer of 2018, represents additional daily natural gas load of roughly 7.5 – 9.5 % when compared against 2017 demand.

Year to date, production volumes in the U.S. have averaged approximately 6 Bcf per day higher than volumes in 2017 so the market should have ample supply despite the increase in demand. However, as the supply and demand factors fluctuate throughout 2018, forward prices will react accordingly. Those movements in natural gas prices will flow through to impact power prices as natural gas and power prices are highly correlated.

At AEP Energy we have the resources to keep you informed with conditions affecting your energy prices. Are you on the right path? Contact us today to develop your energy strategy.

Market Overview – AEP Energy Trading

Natural Gas

During the month of March, natural gas and power prices

were able to push higher throughout the curve as a result of

persistently below normal weather for much of the eastern

half of the country.

Prompt month (April 2018) natural gas at Henry Hub moved up

$0.066/MMBtu to close at $2.733/MMBtu.

Balance of the year (May – December 2018) was up slightly by

$0.050/MMBtu to $2.846/MMBtu.

Beyond that, Calendar 2019 was up $0.014/MMBtu to

$2.791/MMBtu, and Calendar 2020 down $0.023/MMBtu

to $2.775/MMBtu.

Power PJM – Ohio

April 2018 AEP – Dayton Hub peak power jumped up

$2.15/MWh to settle at $35.50/MWh.

May 2018 AEP – Dayton Hub peak power was up $1.25/MWh

to $35.40/MWh.

Balance of the year (May – December 2018) climbed

$0.75/MWh to $35.47/MWh.

In the calendar years, 2019 increased $0.69/MWh to

$34.69/MWh and 2020 increased $0.65/MWh to

$34.37/MWh.

Power Illinois

PJM ComEd zone March 2018 day-ahead peak power closed

$28.22/MWh, climbing $1.47/MWh from February’s close.

MISO Illinois.Hub March 2018 day-ahead peak power closed

$26.56/MWh, up slightly by $0.08/MWh from

February’s close.

Power MISO

FERC approved the request of MISO Transmission Owners’

who have forward-looking transmission formula rates, revising

their rates to reflect the tax changes effective back to January

1, 2018. The tax change reflects the reduced tax rate of 21%

down from 35% as a result of the Tax Cuts and Jobs Act.

The affected MISO Transmission Owners with forward-

looking transmission rate formulas filed a waiver request

with FERC to allow revisions to their 2018 projected net

revenue requirements reflecting the new federal corporate

tax rate.

Without the waiver, transmission owners would not have

been able to implement the new federal tax rate until 2019,

requiring a true-up for 2018, which in turn, customers would

see in 2020 transmission rates.

MISO expects to implement revised transmission rates during

March 2018 and re-bill transmission rates for January and

March 2018.

Any references made to prompt month natural gas will normally be associated with a range starting the first day of the month through the final settlement of the respective prompt month natural gas contract. Other references to forward natural gas prices and all power prices will be based on a range starting the first day of the month through the final day of the month.

AEP Energy does not guarantee the accuracy, timeliness, suitability, completeness, freedom from error, or value of any information herein. The information presented is provided “as is”, “as available”, and for informational purposes only, speaks only to events or circumstances on or before the date it is presented, and should not be construed as advice, a recommendation, or a guarantee of future results. AEP Energy disclaims any and all liabilities and warranties related hereto, including any obligation to update or correct the information herein. Summaries and website links included herein (collectively, “Links”) are not under AEP Energy’s control and are provided for reference only and not for commercial purposes. AEP Energy does not endorse or approve of the Links or related information and does not provide any warranty of any kind or nature related thereto.

From an initial pilot program to a complete fleet conversion, following these best practices will ensure a smooth ride on your sustainability journey. (3-minute read) Building an electric school bus fleet involves several critical steps to ensure efficiency, safety, and environmental impact. AEP Energy recently brought together school administrators and transportation directors for thought provoking …

(2 minute read) Stakeholder demands for sustainability and decarbonization are driving the need for companies to meet emission reduction targets. Are you challenged by how to successfully meet your goals, while also balancing cost and reliability? Building a decarbonization roadmap gives you a step-by-step process to manage roadblocks and meet greenhouse gas emission reduction targets. …

Enter your zip code to see energy plans in your area

Already an AEP energy customer?Login to view account details or enroll at the same rate as new customers.

We found several utilities in your area! Please select yours below:

AEP Energy Reward Store is filled with a variety of energy-saving products for your home. It is a simple and convenient way for you to shop for items to make your home more energy efficient while saving you time and money.

Collect Reward Dollars each month ($5/electric, $3/natural gas) for simply being an AEP Energy Customer.

Shop AEP Energy Reward Store for energy-efficient products like smart thermostats, LED lighting, and more.

Redeem your accumulated Reward Dollars and enjoy smart solutions for your home.

We're Sorry

Brandi Nye, Managing Director of Business Solutions

Brandi is an expert in her field with professional experience in the sustainability industry. Not only does Brandi have solid base knowledge, but she continues to grow her acumen through various learning and development experiences. Brandi is a creative and thoughtful utility professional with expertise in regulatory and utility operations.