December 2017 Edition: Real-Time vs. Day-Ahead Pricing

LMP-based product structures have become referred to as “index”, centered around two major themes Day-Ahead and Real-Time LMP. In this edition, we explore the differences between these two hourly indexes.

To Day-Ahead, or Real-Time, that is the question?

Since the opening of the first competitive retail electric markets, there has been an ever growing and evolving set of product offerings. Electric supply products are continuously reshaped to meet morphing regulatory climates, fluctuating markets, and the shifting strategies of both the suppliers and end-use consumers.

In the earlier days of retail choice, products focused on guaranteed savings against utility default service rates, but as markets grew and competition heightened a plethora of new products were introduced to meet the growing needs of the customer. A greater number of customers began exploring lower cost, market-based products, intent on energy settling hourly against the physical clearing price of power, also known as the Locational Marginal Pricing (LMP). This structure was akin to the settlements of the wholesale market participants selling and buying power on the bulk power system. The settlement of the deregulated energy markets is the responsibility of the Independent System Operator (ISO) who acts somewhat like a clearing house between the generation and load. These LMP-based product structures became commonly referred to as “index”.

Index products at first glance might seem daunting, but center around two major themes: Day-Ahead (DA) and Real-Time (RT) LMP. In this edition, we explore the differences between these two hourly indexes.

Understanding the difference between Day-Ahead and Real-Time prices first requires a cursory understanding of LMP. A version of LMP has been adopted across all deregulated markets and is the primary determinant for settling both energy purchases and sales in the physical Day-Ahead and Real-Time power markets. LMP represents the cost to serve the next megawatt of system load, using the lowest production cost of all available generation. This means the last bid of supply needed to meet the last unit of demand sets the LMP for all megawatts of power delivered for the hour.

The LMP consists of three components, all with their own settlement.

The system energy price is the marginal cost of energy as established by the ISO’s economic (least-cost) dispatching.

Transmission congestion represents the cost of binding constraints within the transmission system.

Transmission losses represent the cost of transmission-related losses at the individual pricing points.

The congestion and losses components are what make LMP unique from one pricing point (i.e. node) to the next. The raw system energy price will always be the same across the system.

LMP is settled twice, once in the Day-Ahead market and again in the Real-Time. This is known as a two-settlement (multi-settlement) system design. In a multi-settlement system, two successive runs of LMP are cleared with the first run occurring the day prior to the operating day, appropriately named the Day-Ahead energy market. In the Day-Ahead market, generators offer supply while Load Serving Entities (LSE) bid demand. The ISO will commit the lowest cost generators based on the required demand producing 24-hourly clearing prices. This provides generators ample notice of their generation expectations for the next operating day while also providing some price certainty to the load. Since the Day-Ahead market is modeled based on optimal operating conditions, less price volatility is to be expected within the Day-Ahead clearing prices. The vast majority of system load is committed in the Day-Ahead market.

The second LMP run occurs as each individual hour approaches during the operating day. This is referred to as the Real-Time market. The Real-Time market acts as a balancing market where the day-ahead commitments are balanced against actual demand and system constraints. The generation offers are updated and used to make Real-Time dispatching decisions. This second run of LMP will also produce 24-hourly clearing prices. The Real-Time prices are not known until the full hour has passed. A higher amount of price volatility can occur in the Real-Time market as dispatching is adjusted to the Real-Time system load and outages. When the two-settlement system is performing well, the Real-Time price will clear similar to the Day-Ahead. This means there will be less of a price spread between the Day-Ahead and Real-Time market prices. In the event that the system was not optimally modeled, a greater amount of price variance will occur. This is known as the Day-Ahead Real-Time spread or DART. When these price differentials occur, it can be more advantageous for the load to settle in one market versus the other.

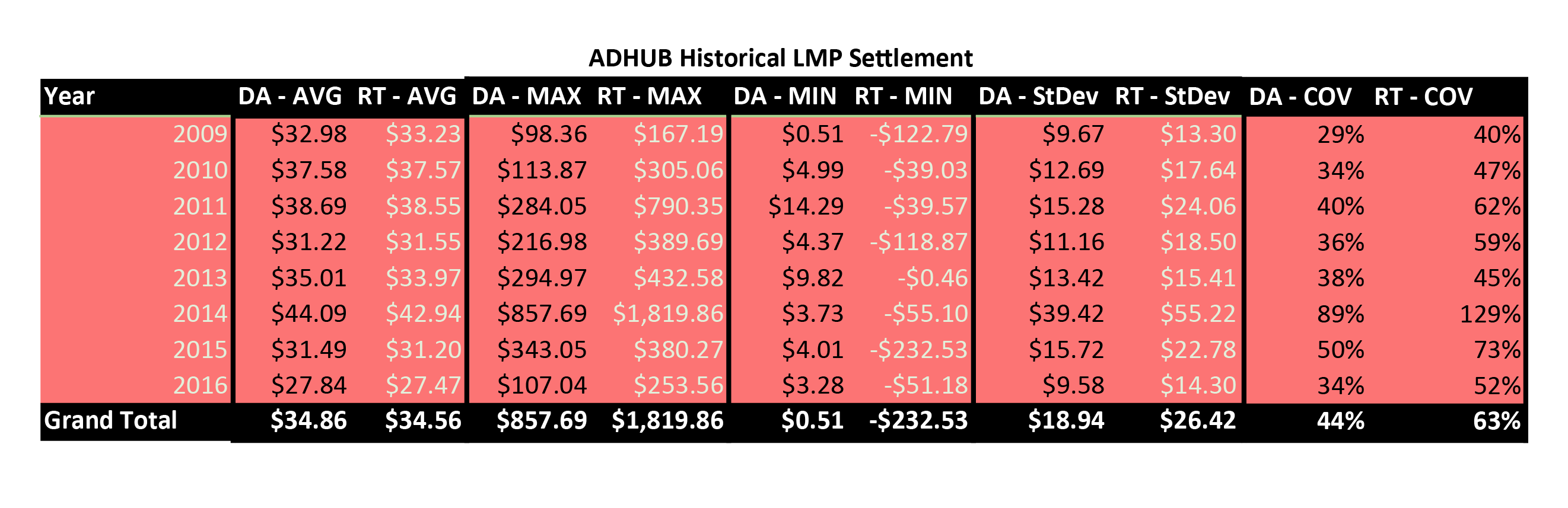

Figure 1 shows the historical around-the-clock calendar year averages for both the Day-Ahead and Real-Time prices settled at the AEP-DAYTON HUB. On average Real-Time prices cleared lower than the Day-Ahead but also suggested by the table is a much greater amount of price volatility within the Real-Time market. It is important to note this table, which is calculated using straight averages, takes no consideration of on-peak versus off-peak consumption. Real-Time prices tend to be even more volatile across the on-peak hours. Customers whose load is weighted more heavily to the on-peak will have a greater amount exposure to Real-Time price spikes when settling in the Real-Time market. The max clearing prices seen in Figure 1 provide some visibility into how severe these price spikes can be. Figure 1: Historical DA vs RT LMP settlements at AEP-Dayton HUB

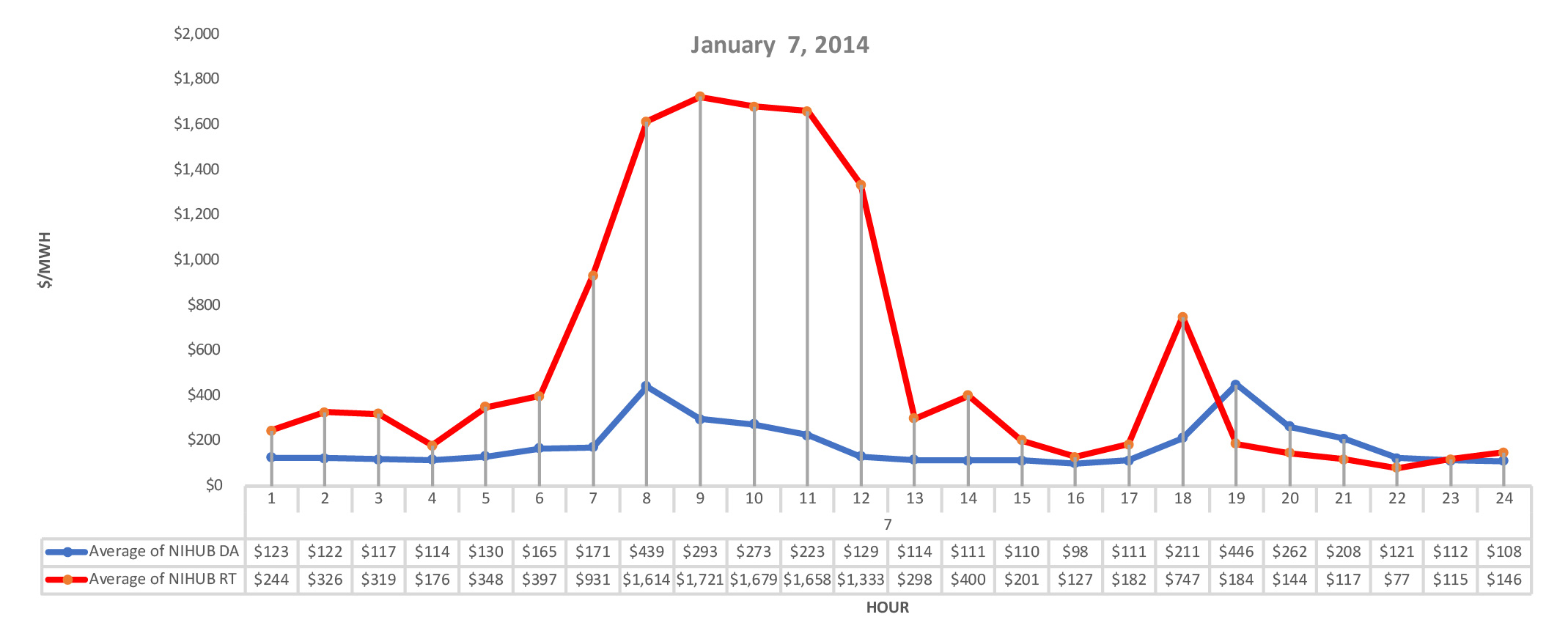

However, Figure 1.2 helps illustrate how much price separation can exist between the two markets. This real-life example is of an operating day during the 2014 Polar Vortex in which Real-Time prices were observed at a premium greater than $1,000/MWh above the Day-Ahead clearing price. This helps to highlight the occasional perils of Real-Time index product structures.

Figure 1.2: Northern IL HUB DA & RT prices January 7, 2014 – Polar Vortex

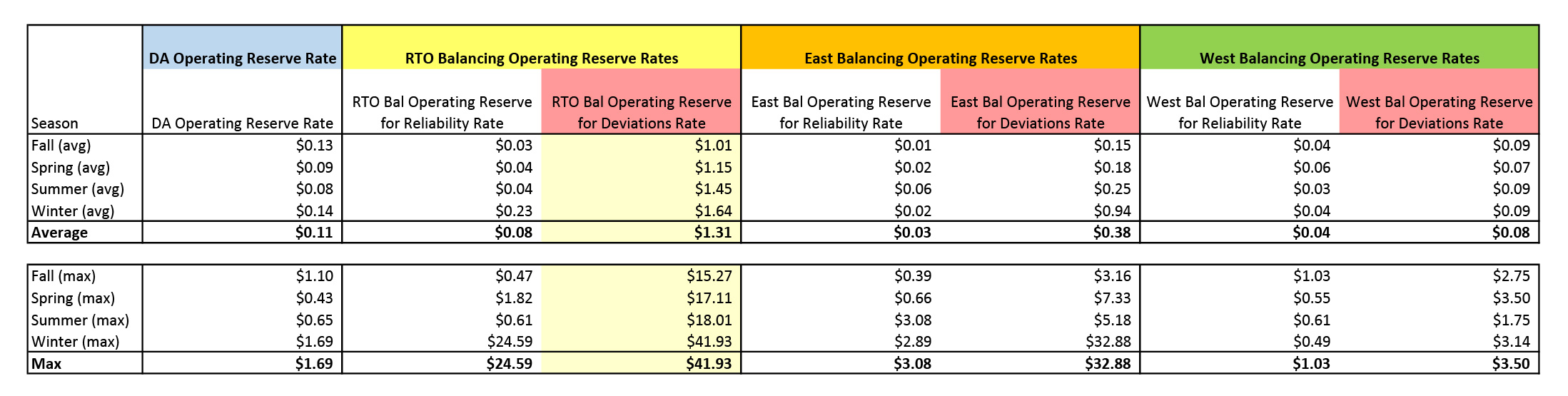

When evaluating Day-Ahead or Real-Time products it is imperative to understand the additional ancillary costs associated with both markets. Not always will lower clearing prices in one market versus the other result in a lower net settlement of cost when it comes to calculating a retail invoice. The customer must also consider the impact of operating reserves, and how these additional ancillary costs are structured within their respective retail agreements. Day-Ahead load is subject to Day-Ahead operating reserves which apply to all load scheduled in the Day-Ahead market. The Day-Ahead operating reserves are meant to reserve a small portion of lower cost and more reliable generation for use in the Real-Time. Energy balanced in the Real-Time market is also subject to a deviation penalty, which is a part of the Balancing Operating Reserves (BOR) charges. These deviation charges can be punitive and act as incentive for load to be committed in the Day-Ahead market. When evaluating the net benefit of one market versus the other it is important to account for the added cost associate with Operating Reserves.

The Operating Reserves rates seen in Figure 2 show the historical average $/MWh settlement of both the Day-Ahead and Balancing Operating Reserves. The Day-Ahead Operating Reserves seen in the first column, which again are only subject to the Day-Ahead load, are incremental to the Day-Ahead LMP settlement price. This cost has averaged around $0.11/MWh historically across the PJM system. BOR, which has added complexities due to regional implications, get broken into two main cost buckets, one for reliability and the other for deviation. The Reliability piece is subject to all system load regardless of which market settlement was elected. The Deviation rates are subject only to the Real-Time and is by far the most punitive of the Operating Reserve charges. These deviation premiums, which again are incremental to LMP, have historically settled at $1.31/MWh within the PJM System. This would imply that the hourly Real-Time price would need to be at minimum $1.31/MWh lower for there to be a cost advantage over Day-Ahead. During the most extreme operating days BOR Deviation rates have been observed as high as $41.93/MWh. To avoid unexpected costs, it is important to understand how these Operating Reserve costs are factored into your retail index agreement.

Figure 2: PJM Operating Reserve Data

In conclusion, index products can provide customers with both access and transparency into the physical power markets which have historically been reserved for wholesale market participants. Index contracts can be structured in a multitude of ways, however the most common involve settling energy 100% to either the Day-Ahead LMP or Real-Time LMP. Lastly, the implication of Operating Reserve rates must be considered and clearly addressed within the purchasing agreement. It is important for you to understand the implications of both markets prior to electing one index product over the other. Customers who have a greater risk appetite may have the ability to capture lower wholesale prices by electing an energy contract priced to the LMP. However, those with high load-to-price correlation will be more vulnerable to Real-Time price spikes. Your AEP Energy expert is here to help you become familiar with your business’ load shape to better gauge your overall exposure in one market versus the other. Call us today to learn more.

Market Overview – AEP Energy Trading

Natural Gas

Following steep declines during the month of October, prices stabilized in November 2017 as the prospects for a cold December provided support for both natural gas and power.

Prompt month (January 2018) natural gas was close to unchanged at $3.025/MMBtu.

All of Calendar year 2018 eked out a half penny gain to close at 2.959/MMBtu.

Further out in the curve, Calendar year 2019 slipped by

$0.016/MMBtu to close at $2.884/MMBtu.

Power PJM – Ohio

In power, colder forecasts pushed December 2017 on-peak AEP – Dayton Hub higher by $2.40/MWh settling to $36.50/MWh.

Winter prices (January through February 2018) actually declined $1.39/MWh down to $39.25/MWh.

Despite winter being off, all of Calendar year 2018 finished higher by $0.16/MWh closing at $35.76/MWh, whereas Calendar year 2019 was up $1.16/MWh to $35.33/MWh on PJM’s proposal to enhance price formation by allowing inflexible units to set Locational Marginal Prices (LMP).

Contact your AEP Energy sales representative to learn more about PJM’s proposed enhancements to Energy Price Formation.

Power Illinois

PJM ComEd zone November 2017 day-ahead on-peak closed$31.78/MWh, up $0.97/MWh from October’s close.

MISO Illinois.Hub November 2017 day-ahead on-peak closed$28.87/MWh, dipping by $1.34/MWh from October’s close.

Any references made to prompt month natural gas will normally be associated with a range starting the first day of the month through the final settlement of the respective prompt month natural gas contract. Other references to forward natural gas prices and all power prices will be based on a range starting the first day of the month through the final day of the month.

AEP Energy does not guarantee the accuracy, timeliness, suitability, completeness, freedom from error, or value of any information herein. The information presented is provided “as is”, “as available”, and for informational purposes only, speaks only to events or circumstances on or before the date it is presented, and should not be construed as advice, a recommendation, or a guarantee of future results. AEP Energy disclaims any and all liabilities and warranties related hereto, including any obligation to update or correct the information herein. Summaries and website links included herein (collectively, “Links”) are not under AEP Energy’s control and are provided for reference only and not for commercial purposes. AEP Energy does not endorse or approve of the Links or related information and does not provide any warranty of any kind or nature related thereto.

From an initial pilot program to a complete fleet conversion, following these best practices will ensure a smooth ride on your sustainability journey. (3-minute read) Building an electric school bus fleet involves several critical steps to ensure efficiency, safety, and environmental impact. AEP Energy recently brought together school administrators and transportation directors for thought provoking …

(2 minute read) Stakeholder demands for sustainability and decarbonization are driving the need for companies to meet emission reduction targets. Are you challenged by how to successfully meet your goals, while also balancing cost and reliability? Building a decarbonization roadmap gives you a step-by-step process to manage roadblocks and meet greenhouse gas emission reduction targets. …

Enter your zip code to see energy plans in your area

Already an AEP energy customer?Login to view account details or enroll at the same rate as new customers.

We found several utilities in your area! Please select yours below:

AEP Energy Reward Store is filled with a variety of energy-saving products for your home. It is a simple and convenient way for you to shop for items to make your home more energy efficient while saving you time and money.

Collect Reward Dollars each month ($5/electric, $3/natural gas) for simply being an AEP Energy Customer.

Shop AEP Energy Reward Store for energy-efficient products like smart thermostats, LED lighting, and more.

Redeem your accumulated Reward Dollars and enjoy smart solutions for your home.

We're Sorry

Brandi Nye, Managing Director of Business Solutions

Brandi is an expert in her field with professional experience in the sustainability industry. Not only does Brandi have solid base knowledge, but she continues to grow her acumen through various learning and development experiences. Brandi is a creative and thoughtful utility professional with expertise in regulatory and utility operations.

However, Figure 1.2 helps illustrate how much price separation can exist between the two markets. This real-life example is of an operating day during the 2014 Polar Vortex in which Real-Time prices were observed at a premium greater than $1,000/MWh above the Day-Ahead clearing price. This helps to highlight the occasional perils of Real-Time index product structures.

However, Figure 1.2 helps illustrate how much price separation can exist between the two markets. This real-life example is of an operating day during the 2014 Polar Vortex in which Real-Time prices were observed at a premium greater than $1,000/MWh above the Day-Ahead clearing price. This helps to highlight the occasional perils of Real-Time index product structures.