What the 2028/2029 PJM Capacity Auction Means for Commercial & Industrial Energy Customers

CommercialJul 15, 2026

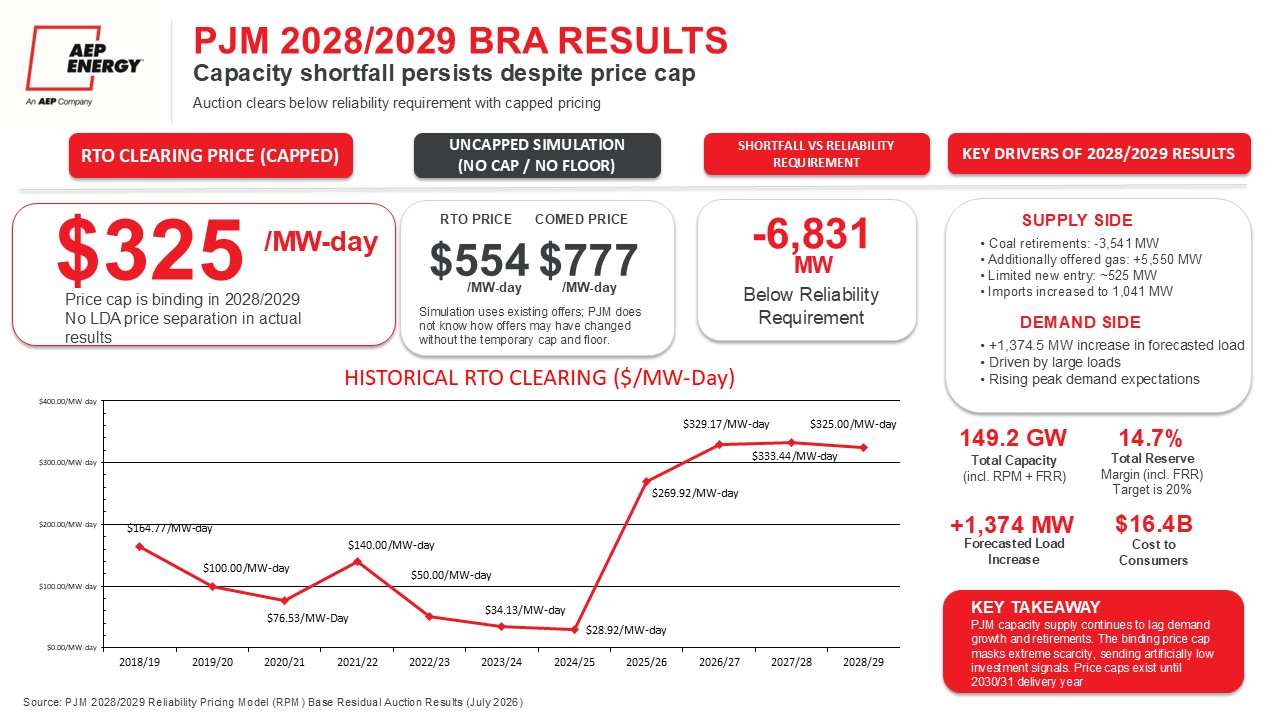

The results of PJM’s latest Base Residual Auction (BRA) send a clear message to commercial and industrial (C&I) energy users: capacity costs are likely to remain a significant component of electricity bills, and underlying market fundamentals continue to point toward a tighter supply-demand balance. PJM secured 138,317.8 MW of capacity for the 2028/2029 delivery year at a clearing price of $325/MW-day, slightly below the prior year’s capped auction result of $333.44/MW-day. Despite the modest decrease, the auction once again cleared at the price cap, highlighting continued scarcity in the PJM market.

Capacity Prices Remain Historically High

After clearing below $35/MW-day during the 2023/2024 and 2024/2025 auctions, PJM capacity prices jumped dramatically beginning with the 2025/2026 auction and have remained elevated ever since. The latest auction will result in approximately $16.4 billion in capacity commitments across the PJM footprint, matching the prior auction despite the slight reduction in price.

What this means for customers: Capacity costs will continue to represent a meaningful share of electricity expenditures. Businesses with large demand profiles should expect capacity management strategies to remain an important component of their energy procurement plans.

The Underlying Market Is Tighter Than the Price Suggests

PJM conducted a simulation showing that without the temporary auction price cap and floor, the market would have cleared at approximately $554.72/MW-day—more than 70% higher than the actual clearing price. In COMED, the simulated clearing price would have reached $776.69/MW-day.

While PJM noted that supplier bidding behavior could have changed without the cap, the simulation demonstrates that fundamental scarcity continues to exist within the market.

What this means for customers: The current auction mechanism is helping moderate price volatility, but the supply-demand imbalance has not disappeared. Businesses should view current capacity costs as being artificially constrained rather than fully reflective of market fundamentals.

Reliability Margins Continue to Shrink

The auction results also revealed that total procured capacity—including Fixed Resource Requirement (FRR) resources—fell 6,831 MW short of PJM’s reliability requirement. The resulting reserve margin was 14.7%, substantially below PJM’s target Installed Reserve Margin of 20%.

This marks the second consecutive auction in which PJM reported a significant capacity shortfall. PJM has stated that this does not mean reliability problems are inevitable, but it does mean the grid would operate with slimmer reserves and higher risk during periods of extreme demand or unexpected outages.

What this means for customers: Grid reliability is becoming increasingly valuable. Programs that reward flexibility, demand response participation, and peak-load reduction may become more important as PJM seeks additional resources to support reliability.

Load Growth Is Accelerating

PJM reported an increase of approximately 1,375 MW of forecasted load, driven largely by growth in large-load customers. Although PJM did not specifically identify data center demand, much of the regional conversation around electricity growth continues to focus on the expansion of AI, cloud computing, and hyperscale data centers.

At the same time, reserve margins remain below target levels, creating a challenging dynamic in which demand growth is occurring faster than new generation resources are being added.

What this means for customers: Companies should anticipate continued upward pressure on capacity costs as economic growth, electrification, and data-center development place additional strain on the regional grid.

Natural Gas Continues to Do the Heavy Lifting

Looking at fuel mix trends, natural gas posted the largest increase in both offered and cleared capacity, while coal capacity continued to decline due largely to planned retirements. Renewable and storage resources also increased, but not at a pace sufficient to offset the loss of retiring conventional generation.

Meanwhile, PJM procured just 524.7 MW of new generation and uprates, down from 774.3 MW in the previous auction. Demand response participation also declined by roughly 300 MW year over year.

What this means for customers: The market still needs significant new supply, transmission investment, demand response participation, and generation development to restore more comfortable reserve margins.

Demand Management Remains One of the Best Tools Available

One of the clearest themes from the auction is the continued value of demand response and peak load management.

Demand response resources successfully cleared approximately 7,000 MW of capacity. In fact, AEP’s territory cleared more than 1,220 MW of demand response capacity, the highest among PJM zones.

What this means for customers: Organizations should evaluate:

Peak demand reduction strategies

Demand response participation

Energy efficiency investments

Load shifting opportunities

Capacity pass-through programs

Long-term risk management strategies

Bottom Line

The headline from the 2028/2029 BRA is not that prices fell slightly—it is that the PJM market remains fundamentally tight.

A capped clearing price of $325/MW-day, a reserve margin below target levels, continuing capacity shortfalls, growing large-load demand, and limited additions of new generation all point to ongoing pressure on future capacity costs.

For commercial and industrial energy users, the winning strategy is no longer simply buying power at the lowest commodity price. Success increasingly depends on actively managing demand, understanding capacity exposure, and developing a long-term energy strategy that accounts for a rapidly evolving PJM market. Contact your AEP Energy sales representative to discuss ways your organization can mitigate the impact of elevated capacity costs even when market-wide auction results remain high.

AEP Energy does not guarantee the accuracy, timeliness, suitability, completeness, freedom from error, or value of any information herein. The information presented is provided “as is”, “as available”, and for informational purposes only, speaks only to events or circumstances on or before the date it is presented, and should not be construed as advice, a recommendation, or a guarantee of future results. AEP Energy disclaims any and all liabilities and warranties related hereto, including any obligation to update or correct the information herein. Summaries and website links included herein (collectively, “Links”) are not under AEP Energy’s control and are provided for reference only and not for commercial purposes. AEP Energy does not endorse or approve of the Links or related information and does not provide any warranty of any kind or nature related thereto.

As energy markets evolve, understanding the forces behind your electricity costs is more important than ever. AEP Energy’s Understanding Capacity Series is a must-watch for businesses looking to stay ahead of the curve and make informed energy decisions in the face of rising capacity costs. What’s in the Series? This insightful video series features AEP …

3 min read Let’s talk about something that’s making waves in the energy sector: demand management. Specifically, how it can help businesses navigate the rising capacity prices in PJM. Whether you’re a business owner or an operations manager, you’ll want to pay attention to this. What is Demand Management? Demand management is a strategy where …

Enter your zip code to see energy plans in your area

Already an AEP energy customer?Login to view account details or enroll at the same rate as new customers.

We found several utilities in your area! Please select yours below:

AEP Energy Reward Store is filled with a variety of energy-saving products for your home. It is a simple and convenient way for you to shop for items to make your home more energy efficient while saving you time and money.

Collect Reward Dollars each month ($5/electric, $3/natural gas) for simply being an AEP Energy Customer.

Shop AEP Energy Reward Store for energy-efficient products like smart thermostats, LED lighting, and more.

Redeem your accumulated Reward Dollars and enjoy smart solutions for your home.