After a year of unprecedented events, the start of 2021 gives us a chance to check in on trends in the energy markets. Last year saw significant shifts in load, dips and spikes in natural gas prices, all-time low spot prices in the PJM power market, and an accelerating shift in the electricity generation mix. We have discussed many of these topics in-depth in prior editions of Customer Insights, so today we take a step back to assess what happened, what changed, what held steady and what we expect during 2021.

What Happened

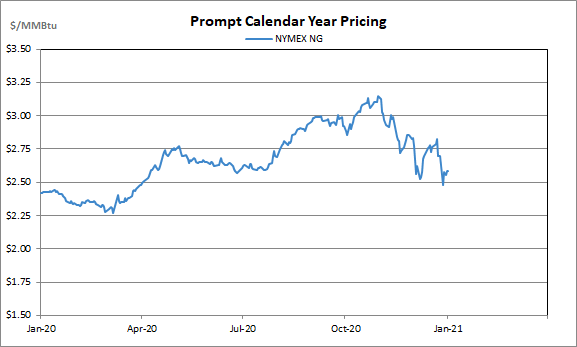

Even before the COVID-19 pandemic, we came into 2020 awash in cheap natural gas. Prices below $2.00/MMbtu did not seem sustainable at the time and then consumption dropped, driving prices even lower. Production eased, especially in associated gas (which is a byproduct of oil production), and concerns about a whiplash in the market grew. Prices were bid up in the fall on concerns of scarcity, but weather was mild and storage stayed high. Overall, the reduction in natural gas production that we saw in 2020 feels like a right sizing as opposed to a temporary shock. According to U.S. Energy Information Administration (EIA) data, total U.S. production on average from March through October 2020 was down on average only 7% from the high in December 2019.

Exhibit A: NYMEX Natural Gas – Prompt Calendar Year Pricing

This easing of production was in response to reduced demand, which we saw on the electricity side as well. In 2019, we thought it was remarkable that, after January, not a single month saw the average locational margin price (LMP) at AEP-Dayton Hub exceed $30/MWh. Fast forward to 2020 and we saw the same average monthly LMP stay below $20/MWh from March through June, and the average for the year was well below $25/MWh. Electricity consumers with index agreements have benefited greatly from these low prices in the spot market.

What Changed

As daily life changed, power consumption patterns shifted. Commercial loads were down and residential loads were up as a significant portion of the workforce moved to remote work. According to PJM, overall energy usage appears to have been down in the spring and fall as part of this shift, while overall usage in the summer came in near forecast levels. It remains to be seen whether some aspects of the economy have been permanently altered by the changes brought about by the pandemic, but we will be keeping an eye on emerging energy consumption patterns.

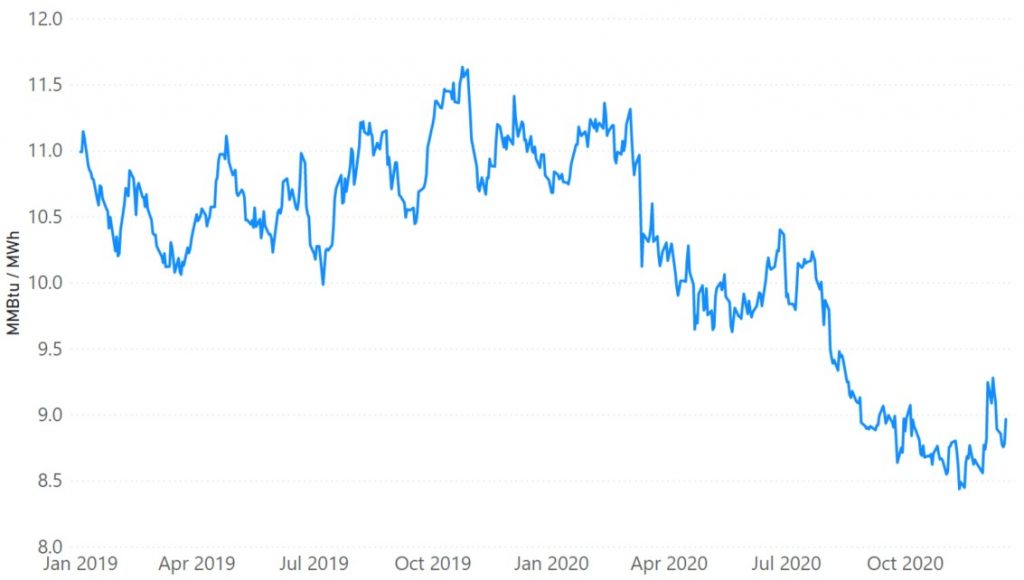

A more nuanced, but meaningful change has happened with heat rates in PJM. A heat rate, measured in MMBtu/MWh, is the amount of natural gas needed to generate a MWh of electricity. To determine the system-wide heat rate, you divide the power price by the natural gas price. By examining heat rates and how those move over time, we can gain some insight into power market fundamentals independent of underlying fuel price (e.g. natural gas) influences. Throughout 2019, the forward 12-month heat rate fluctuated between 10 and 11. In 2020, we saw the implied heat rate slide down and level off in the 8.7 range. Given the number and diversity of generation sources in PJM, that is a meaningful deterioration in heat rates. Likely explanations for the trend in heat rates include coal retirements, renewable additions and the fact that with decreased loads in 2020, the zero marginal cost renewable and nuclear generators were lifted in the supply bid stack while the higher cost fossil generation units were not.

Exhibit B: PJM Implied Heat Rate

What Held Steady

The long-term view of the power market in PJM has remained consistent throughout the uncertainty that we have seen in the near-term. The consensus view of power markets has been that prices will remain low in the coming months until the economy fully reopens. In the medium term, 12 to 18 months, prices are expected to rise as supply catches up to demand. Finally, in the longer term, 24 months and beyond, prices are expected to be slightly lower, as markets return to the pre-pandemic view that energy prices are likely to continue to trend flat to slightly down. The only thing that has not remained steady about this view is the starting point – markets are waiting along with the rest of the economy.

While the view on downward trending energy has held steady, so too has the view on upward trending transmission costs. Transmission investment is based on decades long projections and has not been impacted significantly by the slowdown. Continued investment in the transmission system is seen as critical to achieving the levels of renewable generation that many states and utilities have targeted, so it is likely that transmission costs to customers will continue their steady climb.

What We Expect

Last spring, it felt like the market was oversold. This fall, prices felt like they were bid up a little too high. Going forward, it feels like we are back on solid footing in the power markets after some movement that may not have been entirely guided by fundamentals. With no clear bias toward upward or downward movement, the markets will likely be driven by weather for the remainder of the winter – a winter that so far has proven to be mild.

Despite this mild start, though, we have plenty of experience in the last decade to remind us how volatile winter weather and winter energy pricing can be. The polar vortex and bomb cyclone events we have seen over the past decade drove LMPs to double and triple normal levels. A clear trend that solidified in the 2010s and shows no sign of changing is that substantial price volatility in PJM is concentrated in the winter months.

We expect to see continued renewable generation growth in the PJM region. PJM has lagged behind other regions of the county in wind and solar build out, but the economics have tipped clearly in this direction. Coal generation will continue to be phased out, and while natural gas will likely continue to dominate PJM generation for the coming decade, it seems likely that additions will be mostly renewable.

What You Can Do

As energy markets reset heading into 2021, now is a great time to consider your energy strategy and determine whether you need a reset. Our previous Customer Insights editions are a great way to help you on a new energy strategy path for 2021. Understand your renewable energy options, learn how spot vs. forward buying strategies can benefit your organization and find out how the cost of generating energy has continued to evolve. If you are still approaching energy the same way you always have, now’s the time for your strategy to evolve.

Interested in learning more? If you are interested in learning more about AEP Energy’s view on market trends or how your organization might take advantage of new opportunities to unlock value in your energy spend, contact Evan Howell, Director, Energy Services for AEP Energy, at ehowell@aepenergy.com or call Evan at 312-488-2211. If you are already working with an AEP Energy Sales Representative, they will happily provide more information.

AEP Energy does not guarantee the accuracy, timeliness, suitability, completeness, freedom from error, or value of any information herein. The information presented is provided “as is”, “as available”, and for informational purposes only, speaks only to events or circumstances on or before the date it is presented, and should not be construed as advice, a recommendation, or a guarantee of future results. AEP Energy disclaims any and all liabilities and warranties related hereto, including any obligation to update or correct the information herein. Summaries and website links included herein (collectively, “Links”) are not under AEP Energy’s control and are provided for reference only and not for commercial purposes. AEP Energy does not endorse or approve of the Links or related information and does not provide any warranty of any kind or nature related thereto.

(2 minute read) Stakeholder demands for sustainability and decarbonization are driving the need for companies to meet emission reduction targets. Are you challenged by how to successfully meet your goals, while also balancing cost and reliability? Building a decarbonization roadmap gives you a step-by-step process to manage roadblocks and meet greenhouse gas emission reduction targets. …

(2 minute read) Transmission Rates Keep Climbing Have you noticed the transmission rate on your energy bill increasing recently? You are not imagining things. In some areas, rates have increased over 75%! Regardless of whether transmission costs are billed by the utility or passed through to you on your retail energy supplier bill, this costly …

Enter your zip code to see energy plans in your area

Already an AEP energy customer?Login to view account details or enroll at the same rate as new customers.

We found several utilities in your area! Please select yours below:

AEP Energy Reward Store is filled with a variety of energy-saving products for your home. It is a simple and convenient way for you to shop for items to make your home more energy efficient while saving you time and money.

Collect Reward Dollars each month ($5/electric, $3/natural gas) for simply being an AEP Energy Customer.

Shop AEP Energy Reward Store for energy-efficient products like smart thermostats, LED lighting, and more.

Redeem your accumulated Reward Dollars and enjoy smart solutions for your home.

We're Sorry

Brandi Nye, Managing Director of Business Solutions

Brandi is an expert in her field with professional experience in the sustainability industry. Not only does Brandi have solid base knowledge, but she continues to grow her acumen through various learning and development experiences. Brandi is a creative and thoughtful utility professional with expertise in regulatory and utility operations.