The Downfall of Coal: Market Rules or Market Forces?

CommercialJan 30, 2018

January 2018 Edition: The Downfall of Coal: Market Rules or Market Forces?

Is it market rules or market forces driving challenges for coal-fired generators? Our industry expert will take a deep dive into these matters to help you better understand the cause and effect on energy prices.

The Downfall of Coal: Market Rules or Market Forces?

Since the opening of the first competitive retail electric markets, there has been an ever growing and evolving set of product offerings. Electric supply products are continuously reshaped to meet morphing regulatory climates, fluctuating markets, and the shifting strategies of both the suppliers and end-use consumers.

In recent years, electricity generation has been a focal point. Coal-fired generation plants have retired at an alarming rate and nuclear power plants struggle to avoid closing, while a flurry of new natural gas power plants are being brought online. What is the driving force behind the challenges coal generators face today? In this edition of Customer Insights, our industry expert will dive deep into these driving forces to help you better understand the cause and the effect on energy prices.

On January 8, 2018 the Federal Energy Regulatory Commission (FERC) rejected a rulemaking directive by the Department of Energy (DoE) to extend a financial lifeline to struggling coal-fired and nuclear plants. Back in September, the DoE in its Notice of Proposed Rulemaking (NOPR) had stated that “the resiliency of the nation’s electric grid is threatened by the premature retirements of power plants”, recommending FERC develop a cost recovery mechanism for fuel-secure generation resources for their resiliency and reliability attributes that are not equitably compensated due to the “chronic distortion” in competitive markets. The DoE went further, quoting an earlier letter to FERC from the chairmen of the Senate and House Committees on Energy that “the broad scale premature retirements of otherwise performing baseload units because of market rules – rather than market forces – would represent a failure of regulation”.

The argument put forth by the DoE, and many others before it, was that the flood of coal plant retirements is a direct consequence of discriminatory market rules – such as environmental regulations and renewable energy subsidies – forcing a rapid decline in coal-fired generation over the past decade that threatens grid reliability and may result in volatility in wholesale power markets. While it is undeniable that the confluence of a number of trends have all contributed, it may be worth exploring if it is regulatory pressures or rather market fundamentals, such as low natural gas prices, that have struck the decisive blow in the downfall of coal. Historical shift

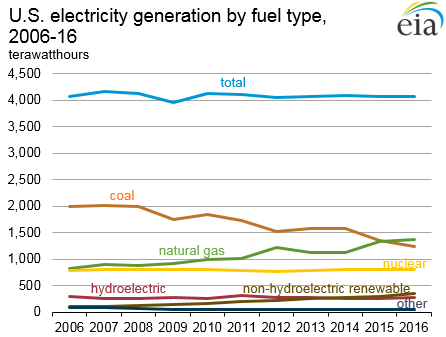

In 2016, natural gas surpassed coal as the leading fuel source for electric generation in the United States for the first time. Approximately 34% of generation was sourced from natural gas plants compared to 30% from coal-fired generators. Between 2006 and 2016, electric generation in the United States has remained roughly flat but the resource mix has dramatically shifted in favor of natural gas.

Source: EIA.gov

Over 40 GW of coal capacity has been retired in the past five years, with 15 GW of capacity shut down in 2015 alone. While there is evidence that the vast majority of capacity taken offline was prompted by looming environmental compliance deadlines, only around 30% of the decrease in generation can directly be attributed to retirements.

The majority of the closures have been of smaller, older and less efficient subcritical units well past their useful lives. The ballooning costs of operating and maintaining this aging subcritical fleet had made them uncompetitive long before some of the onerous environmental regulations, like the U.S. Environmental Protection Agency’s (EPA) Mercury and Air Toxics Standards (MATS) kicked in. MATS, which went into effect in May of 2015, only accelerated the day of reckoning of these uneconomic units.

The rest of the decline in generation is attributable to lower capacity utilization as wholesale power prices have tumbled tracking the price of natural gas closely. The absence of any demand load growth has only exacerbated the problem. This does bode well for the surviving coal fleet, however, as there is a substantial amount of unused capacity that any sustained strength in demand and, in turn, power prices, could result in a rebound in output from coal generators. This was briefly evident during the cold spell that gripped the U.S. during the first week in 2018. Generation from coal-based sources served almost 40% of the total load requirement, nearly twice as much as natural gas units. Energy Pricing

Competitive wholesale power prices are primarily determined by the cost of fuel. Natural gas generators with shorter run times and quick ramping abilities often used at peak times to power the grid play a critical role in determining the marginal unit that sets the price. While there are several other variables, such as operational constraints and non-fuel expenses, cost of the primary fuel and unit heat rate (a measure of efficiency) have the largest influence in marginal cost calculations. Thus, lower natural gas prices lead directly to lower wholesale electricity prices.

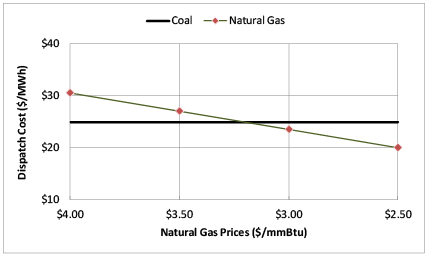

As illustrated in the figure below, a natural-gas combined cycle unit would displace a less efficient subcritical coal-fired unit in dispatch priority as the price of natural gas delivered to the facility falls below $4/MMBtu. As the price of natural gas approaches or dips below $3/MMBtu, a natural gas generator would supplant even the most efficient supercritical coal unit in the dispatch stack. Figure 2: Dispatch cost of a Natural Gas-fired combined cycle unit under various gas prices

This is the price environment coal generators find themselves in today, with natural gas prices having been in the $3/MMBtu range for the past several years. With abundant supplies from the Marcellus and Utica shales and rapid development in pipeline infrastructure to deliver to demand centers, natural gas prices are expected to stay below $4/MMBtu for the foreseeable future. Lower natural gas prices, combined with superior operational flexibility of modern natural gas plants, has alleviated overall power price volatility as well. Capacity Markets

In competitive power markets, generators are also compensated for their availability and reliability through capacity payments. PJM has a mature capacity market that conducts annual auctions three years into the future to ensure adequate supply and reserves to meet anticipated demand. In spite of the market reforms triggered by the squeeze in supply experienced during the polar vortex events of 2014, the absence of any meaningful load growth and entry of 3 – 4 GW of new natural gas combined cycle plants every year, capacity clearing prices in PJM capacity auctions have plummeted. The prices, down from a high of $165/MW Day for the 2018/19 delivery year to $76/MW Day in the most recent auction conducted for planning year 2020/21, suggest a heavily oversupplied market. With greater maintenance and capex requirements in addition to the fixed costs associated with installation and maintenance of the myriad of complex emissions control equipment, coal generators are struggling to survive in the capacity markets as well. King Natural Gas?

In its unanimous rejection of the DoE proposal, FERC categorically rebuffed the DoE’s assertion that the power pricing mechanisms currently in place were fundamentally deficient, adding that, while market dynamics have indisputably swung in favor of natural gas, there appeared to be no immediate threats to the reliability of the bulk electricity system.

The repeal of the Clean Power Plan in October by the EPA, and the current uncertainty around some other impending regulations, has only provided temporary breathing room to coal generators. Even in the absence of any new regulatory policy pressures on coal, the transformation of the power markets driven by the abundance of cheap natural gas supplies appears to be unstoppable. Stay Tuned

AEP Energy’s Customer Insights is published to keep you informed concerning current events. Our goal through AEP Energy’s Customer Insights is to provide educational topics committed to helping you manage your energy procurement.

Market Overview – AEP Energy Trading

Natural Gas

The month of December 2017 saw mixed price changes as mild temperatures during the first three weeks weighed on natural gas.

Significantly below normal temperatures during the last weekof December ignited power prices primarily in the front ofthe curve.

Prompt month (January 2018) natural gas finished at$2.953/MMBtu, down $0.072/MMBtu.

Balance of the year (February – December 2018) settled at$2.836/MMBtu, down $0.117/MMBtu.

Further out in the curve, Calendar year 2019 fell$0.071/MMBtu to close at $2.813/MMBtu.

Power PJM – Ohio

In power, prices were initially lower for December 2017 untilthe last week of the month when demand and liquidationscame in exceedingly strong.

As a result, January 2018 on-peak AEP – Dayton Hub gappedup $12.00/MW to settle at $51.80/MWh.

Remaining winter prices, February 2018 was up$3.35/MWh to $42.00/MWh.

Meanwhile, the balance of the year (March – December 2018)declined with natural gas, closing at $35.21/MWh,down $0.18/MWh.

Calendar 2019 closed at $34.71/MWh, down $0.62/MWh.

Power Illinois

PJM ComEd zone December 2017 day-ahead on-peak closed$32.49/MWh, up $0.71/MWh from November’s close.

MISO Illinois.Hub December 2017 day-ahead on-peak closed$27.57/MWh, down by $1.30/MWh from November’s close.

MISO:

On January 11, 2018, MISO released a study regarding therecent 2018 cold air hitting much of the U.S.,“2018 Artic Cold Snap”

Sustained cold temperatures lingered for a longer period oftime during January more so than during the PolarVortex of 2014.

The highest real-time market price on 1/7/2014 hit$1,780.70/MWh whereas the highest real-time market priceon 1/2/2018 reached $281.23/MWh

Any references made to prompt month natural gas will normally be associated with a range starting the first day of the month through the final settlement of the respective prompt month natural gas contract. Other references to forward natural gas prices and all power prices will be based on a range starting the first day of the month through the final day of the month.

AEP Energy does not guarantee the accuracy, timeliness, suitability, completeness, freedom from error, or value of any information herein. The information presented is provided “as is”, “as available”, and for informational purposes only, speaks only to events or circumstances on or before the date it is presented, and should not be construed as advice, a recommendation, or a guarantee of future results. AEP Energy disclaims any and all liabilities and warranties related hereto, including any obligation to update or correct the information herein. Summaries and website links included herein (collectively, “Links”) are not under AEP Energy’s control and are provided for reference only and not for commercial purposes. AEP Energy does not endorse or approve of the Links or related information and does not provide any warranty of any kind or nature related thereto.

(2 minute read) Stakeholder demands for sustainability and decarbonization are driving the need for companies to meet emission reduction targets. Are you challenged by how to successfully meet your goals, while also balancing cost and reliability? Building a decarbonization roadmap gives you a step-by-step process to manage roadblocks and meet greenhouse gas emission reduction targets. …

(2 minute read) Transmission Rates Keep Climbing Have you noticed the transmission rate on your energy bill increasing recently? You are not imagining things. In some areas, rates have increased over 75%! Regardless of whether transmission costs are billed by the utility or passed through to you on your retail energy supplier bill, this costly …

Enter your zip code to see energy plans in your area

Already an AEP energy customer?Login to view account details or enroll at the same rate as new customers.

We found several utilities in your area! Please select yours below:

AEP Energy Reward Store is filled with a variety of energy-saving products for your home. It is a simple and convenient way for you to shop for items to make your home more energy efficient while saving you time and money.

Collect Reward Dollars each month ($5/electric, $3/natural gas) for simply being an AEP Energy Customer.

Shop AEP Energy Reward Store for energy-efficient products like smart thermostats, LED lighting, and more.

Redeem your accumulated Reward Dollars and enjoy smart solutions for your home.

We're Sorry

Brandi Nye, Managing Director of Business Solutions

Brandi is an expert in her field with professional experience in the sustainability industry. Not only does Brandi have solid base knowledge, but she continues to grow her acumen through various learning and development experiences. Brandi is a creative and thoughtful utility professional with expertise in regulatory and utility operations.